Dr. Kurt Hohenstein, Curator

Opened December 1, 2011

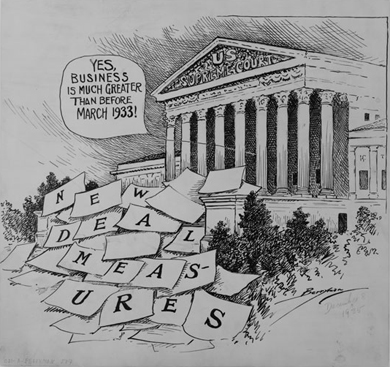

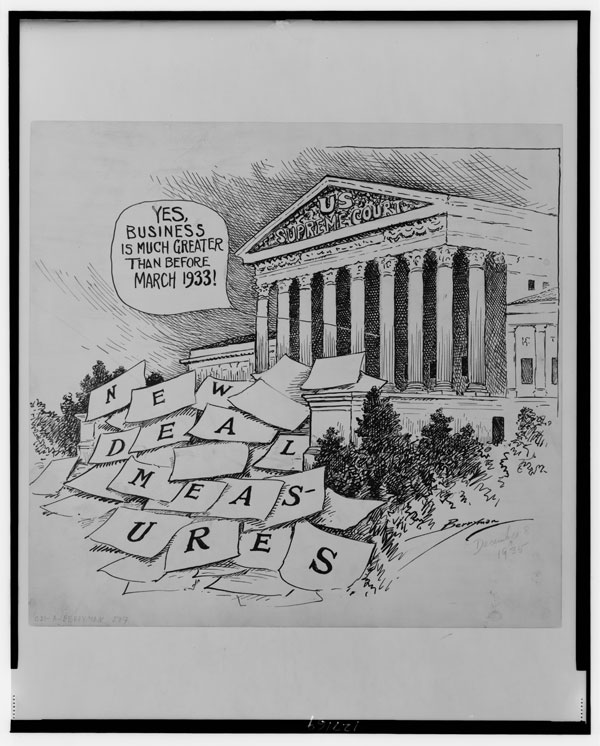

December 8, 1935 - "Yes, business is much greater than before March 1933!"

Soon after his appointment as the second Chairman of the U.S. Securities and Exchange Commission, James Landis, in a speech to the Investment Bankers Association, told the audience that cooperation with the SEC was imperative. “If we (the SEC) fail, others will take charge; their sanctions, their mechanisms, will be different.”1

Landis and William O. Douglas, the SEC’s third Chairman, became the major architects of the SEC’s regulatory and administrative ideology. “Once broad national policies have been established in statutory law,” Douglas said, “the business-government relationship moves out of the realm of controversy and debate…it ceases to be an issue of politics and moves into the province of the technicians.”

The technicians whom Douglas thought should be involved in regulating financial and securities markets were the lawyers of the SEC. Administrative procedure and practice was preferable to court decisions because, he argued, courts were cumbersome, and the administrative process remained informal. “It is easier to plot a way through a labyrinth of detail when it is done in the comparative quiet of a conference room than when it is attempted in amid the turmoil of a legislative chamber or committee room.”

Landis agreed that government needed the support of business and finance. Without administrative procedures that promoted intelligent study and informal compromise, government would be required to so intrude into the details of business that “it becomes a bureaucratic blight.”2

Landis spoke during a time where administrative law predominated. But early securities law developed through court decisions in reaction to an intricate mix of complaints from investors and the general public about market abuses. The nation’s courts, in the context of the federal system, played an instrumental role in the interpretation of securities legislation and administrative implementation. In the early 1900s, that legislation came mostly from the states, which passed laws regulating securities and the markets.

After the stock market crash of 1929, as the regulation of securities became more complex with the passage of the Securities Acts of the New Deal, the newly-established U.S. Securities and Exchange Commission began to interpret the laws, create and implement rules, and develop legal strategies to regulate the securities industry.

The SEC’s legal strategies sought to implement Congressional intent and its own independent regulatory philosophy. SEC lawyers found themselves facing fundamental questions relating to the regulation of the nation’s growing and complex economy. What were the appropriate limits of Congressional power to regulate the markets in the federal system? What was the role and power of the newly-created administrative agency to regulate securities markets and actions? What could the SEC do when the laws passed by Congress were ambiguous or uncertain? And, since the courts were the final arbiters of every controversy, each decision and rule formulated by the SEC posed the ultimate question: what would the courts say?

The story of the development of securities law necessarily involves the written decisions of the courts, but to focus on merely those decisions, those final parchments where the courts give their official opinions and reasoning, ignores much of the story. The context of the case and the decision, the manner by which a case came to be heard by a court, the strategic decisions made by the SEC General Counsel’s Office and appellate legal counsel, the personality of the justices and the court hearing the case, and the legal and economic philosophies of the court all play a part in a court’s decision. Only by considering those factors can the development of securities law as an essential part of our economic history be fully understood and appreciated.

{kind=link}