- 1867 application

By the late 19th century, the New York Stock Exchange (NYSE) had developed such a reputation for exclusivity that its first big competitor, created in 1863, called itself the "Open Board of Stock Brokers." The two rivals soon found much in common, however, and merged.

On May 11, 1869, the reconstituted New York Stock Exchange opened with 1,060 members. The new constitution did away with ad hoc committees and placed all legislative, judicial, and administrative power in a forty-two-member governing committee elected by the full membership. The president and secretary each sat on the governing committee, but they were elected annually. Other committee members were elected for four years, so the governing committee actually wielded more power than the officers. Because the NYSE was a voluntary membership organization, its governing committee could fine, suspend, or expel members at will, even if they were only "guilty of conduct or proceeding inconsistent with just and equitable principles of trade."11

A host of lesser committees were created, including committees on law, arrangements, quotations, commissions, applications, and stock list. Enforcement was split between an arbitration committee that heard disputes regarding contracts, and a business conduct committee that investigated manipulators. Final decisions were left to the all-powerful governing committee, which tended toward leniency, unless the exchange itself was threatened.12

As the exchange's self-regulatory system tackled internal threats, courts helped insulate it from external ones. In 1888, after a member sought judicial review of a NYSE decision, New York's highest court issued a decision in Belton v. Hatch, confirming that the NYSE bore the same relationship to the state as a "private business club." The private business club analogy enabled the NYSE to regulate its members as it saw fit and, as it did in 1899, to compel listed companies to file annual reports and agree to standards of conduct.13

Conduct on the trading floor was transformed during the second half of the 19th century, with the increasing importance of equities trading. Through most of the 1800s, bond trading—first government debt, then railroad bonds—accounted for much of the NYSE's business. But bond trading was generally "order-driven," with the NYSE collecting and matching orders of customers and dealers.

The Open Board had developed a "continuous auction" in which stocks were sold by a specialized seller at a specific location on the floor. Adopted by the NYSE for securities trading, the continuous auction sustained a far greater volume of trading and provided for much faster price discovery. But it also created new regulatory challenges. The key to the system was the "specialist" who occupied a single post and dealt in just one or two stocks, acting alternately as a purchaser of stocks to maintain market activity or as a seller to serve customer demand. The specialist was forbidden to act in both roles at once; he had to give precedence to customers and could not "get out in front" of their orders. Enforcing this separation of duties remained a challenge for years to come.14

The American industrial economy boomed in the late 19th century, and the reinvented New York Stock Exchange took on an aura of permanence and prestige. As America grew up and grew wealthy, the sons of the elite often found their way into the exchange. In April 1903 the NYSE moved into its new Corinthian-columned quarters at Broad and Wall Streets, a suitable home for investors and an institution of immense prestige.15

(11.) May 11, 1869 Transcript of Agreement of Consolidation of New York Stock Exchange and Open Board of Brokers of New York. Membership grew slowly over the next ten years until it was fixed at 1,100.

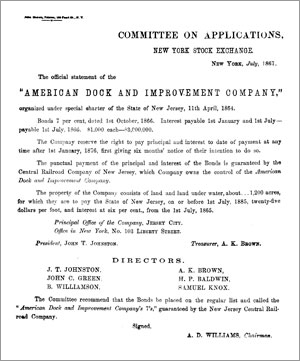

(12.) Meeker, The Work of the Stock Exchange, 449-56; July 1867 Official Statement of the "American Dock and Investment Company" to Committee on Applications, New York Stock Exchange

(13.) Howard C. Westwood and Edward G. Howard, "Self-Government in the Securities Business," Law and Contemporary Politics, Summer 1952, 519-22; Meeker, The Work of the Stock Exchange, 448.

(14.) Bruno Biais and Richard C. Green, "The Microstructure of the Bond Market in the 20th Century," August 29, 2007.

(15.) John Brooks, Once in Golconda: A True Drama of Wall Street, 1920-1938 (New York, 1969), 22.