The Timeline highlights significant developments in the history of financial regulation against U.S. and world events. Choose a different decade below, or scroll down to discover more.

Starting with the Kansas Securities Act in 1911, states adopted a variety of laws to protect investors from fraud and raise capital for business. Some states adjusted the original Kansas law to suit local practice; other states, such as New York with the 1921 Martin Act, set their own securities laws. To establish a uniform system of state securities regulation, the National Conference of Commissioners on Uniform State Laws prepared the Uniform Sale of Securities Act. The Act was adopted in just five states and was abandoned in 1943.

Sponsored by U.S. Senator Reed Smoot (R-UT) and U.S. Representative Willis Hawley (R-OR), the Tariff Act raised the dutiable tariff level on imported goods, in an effort to protect American production. President Hoover signed the legislation against his own preference for international cooperation and in spite of opposition from economists and industrialists. Foreign trading partners retaliated with higher tariffs, and American trade was reduced by half, contributing to the depth and length of the global Depression.

Ultramares Corporation v. Touche confirmed the concept of privity, then an essential requirement of any third-party litigation against accountants based on negligence.

The 1929 crash ended an eight-year bull market fueled by speculation and stock manipulation. By mid-1932, stocks listed on the New York Stock Exchange had lost 83% of their pre-crash value. The U.S. Senate Banking Committee conducted hearings on the crash to determine how to prevent future such occurrences. The hearings were referred to as the Pecora Hearings for Ferdinand Pecora, the Committee's counsel and a future SEC Commissioner.

Congress chartered the Reconstruction Finance Corporation (RFC) to provide aid to state and local governments and loans to banks, mortgage corporations and businesses. The RFC continued under the New Deal to help restore business prosperity. During World War II, the RFC merged with the Federal Deposit Insurance Corporation (FDIC). The RFC closed in 1957.

Adolf A. Berle, Jr. and Gardiner Means published The Modern Corporation and Private Property, a seminal study of the management, ownership and governance of corporations. Their critique, noting that corporate ownership and management was increasingly diverging to the detriment of shareholders, laid the groundwork for future governance initiatives.

Felix Frankfurter, an expert in administrative law at Harvard University Law School, was summoned to Washington to draft what was to become the Securities Act of 1933, with the assistance of James Landis, Benjamin Cohen and Thomas Corcoran. In 1937, Landis was named SEC Chairman. In 1939, Frankfurter was appointed a U.S. Supreme Court Associate Justice. Cohen and Corcoran led major roles in the implementation of the New Deal.

The Securities Act of 1933, enacted on May 27, was the first general federal law to regulate the issuance of securities. The Act required certain issuers of securities to file registration statements with the Federal Trade Commission and to provide a prospectus to investors. The FTC had the power to issue stop orders to prevent the sale of an issuer's securities. The Act set forth the disclosure philosophy that became entrenched in securities laws, and was one of the major pieces of legislation enacted during Roosevelt's first 100 days in office.

The original draft of the Act did not require that financial statements be audited ("certified"). Later drafts considered the value of independent audits, and the feasibility of requiring that audits be made by accountants on staff of the agency that would administer the Act. The bill as passed confirmed the requirement of certification by independent public accountants.

In 1932, the New York Stock Exchange began asking all corporations applying to list securities to agree that published annual financial statements be audited by independent public accountants. The following year, the NYSE required that listing applications include audited financial statements for the most recent fiscal year. By then, over 90% of listed companies had independent audits.

In protest of the Securities Act of 1933, major Wall Street firms refused to bring new issues of stock to the market.

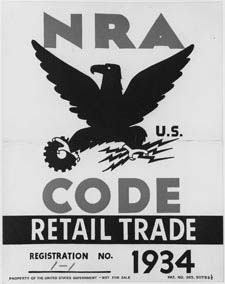

Following creation of the National Industrial Recovery Administration (NIRA), securities dealers created the Investment Bankers Code Committee to promulgate a "code of fair competition" and a "code of fair trading practices" for the industry.

The U.S. Banking Act of 1933, known as the Glass-Steagall Act after its Congressional sponsors - U.S. Senator Carter Glass (D-VA) and U.S. Representative Henry Steagall (D-AL) - limited commercial bank securities activities and affiliations between commercial banks and securities firms, and established the Federal Deposit Insurance Corporation (FDIC) to insure bank deposits with funds from the banks. It was enacted after the failure of nearly 5,000 banks during the Great Depression.

President Roosevelt sent a message to Congress recommending that it pass legislation to regulate the exchanges. U.S. Senator Duncan Fletcher (D-FL) and U.S. Representative Sam Rayburn (D-TX) introduced what was to become the Securities Exchange Act of 1934. Enacted on June 6, the Act required the registration of stock exchanges.

The U.S. Securities and Exchange Commission was created pursuant to the Act. The Act formed the bedrock of the SEC's enforcement and regulatory powers.

Although the 1934 Act did not provide for regional offices, the Commission began planning for them early. On November 12, Joseph P. Kennedy announced the creation of “branches in key cities” expected to be the agency’s enforcement arms. By December,a regional office was operating in New York City, although an administrator had yet to be appointed.

President Roosevelt appointed the first Commission of the U.S. Securities and Exchange Commission, and named Joseph P. Kennedy as the agency's first Chairman. Kennedy had retired from a lucrative career on Wall Street and as a businessman, and was a major contributor to the Democratic Party.

The Boston and Chicago Regional Offices opened on March 1. Within days, Robert G. Page became the first administrator of the New York Regional Office. Offices in Denver, Atlanta, San Francisco, Fort Worth, and Seattle opened later in the year. A Washington Field office, also established in 1935, became a formal regional office in 1942. All regional offices reported directly to the SEC Chairman.

The Public Utility Holding Company Act, enacted on August 26, provided the U.S. Securities and Exchange Commission with the power to limit the size and organization of electricity, natural gas and other utility holding companies. PUHCA eliminated unfair practices by electricity and natural gas companies, including excessive rates, self-dealing and unreliable service. The legislation also called upon the SEC to conduct a study of investment trusts.

In In re American States Public Service Co., a federal court in Maryland held the Public Utility Holding Company Act unconstitutional. Other suits also challenged PUHCA, resulting in inconsistent and conflicting lower court opinions, and preventing the U.S. Securities and Exchange Commission from enforcing the Act.

The U.S. Securities and Exchange Commission opened regional offices in Atlanta, Boston, Chicago, Denver, Fort Worth, New York City, San Francisco and Seattle.

In 1935, J. Edward Jones filed a registration statement with the U.S. Securities and Exchange Commission. Before the statement went into effect, the SEC ordered Jones to show why a stop order should not be issued. Jones sought to withdraw the statement, which the SEC prohibited him from doing. Jones brought a suit challenging the constitutionality of the Securities Act of 1933 and the SEC's refusal to allow him to withdraw. In Jones v. SEC, the U.S. Supreme Court ruled that the SEC must allow him to withdraw. The Court's conservative majority rebuked the SEC, calling its practices akin to the odious "Star Chamber" of England.

The American Society of Certified Public Accountants (ASCPA), formed in 1921 and acting as a federation of state societies, merged with the American Association of Public Accountants (AAPA), founded in 1887. The new group, the American Institute of Accountants (AIA) agreed to restrict future membership to CPAs. In 1957, the organization became the American Institute of Certified Public Accountants; in 2015, it was re-named the American Institute of CPAs.

Mississippi was the first state to issue industrial development bonds, in an effort to use state financing power to build up private industry.

The Revenue Act, backed by investment management firms, accorded special tax treatment to open-ended mutual funds, which the legislation dubbed "mutual investment companies," making them more attractive to investors.

The SEC Office of the Chief Accountant announced that it would issue periodic publications of opinions on accounting principles, towards the development of uniform standards and practice in major accounting questions. The first Accounting Series Release (ASR) was issued in April. ASRs were re-named Financial Reporting Releases (FRR) in 1982, and were later codified as Codification of Financial Reporting Policies (CFRP).

With support from SEC Chairman William O. Douglas, U.S. Senators Joseph O'Mahoney (D-WY) and William Borah (R-ID) submitted a bill mandating federal incorporation of businesses engaged in interstate commerce. While the framers of the Securities Acts intended that such legislation would follow, Congress was unwilling to enact the incorporation bill.

The New York Stock Exchange reorganized its governance structure after the March 7 discovery that Richard Whitney, former president of the Exchange, had embezzled millions. Whitney pled guilty to grand larceny charges and was sentenced to Sing Sing Prison. The U.S. Securities and Exchange Commission held hearings to investigate the extent to which Exchange members were aware of and failed to report Whitney's conduct. The Whitney scandal led to the creation of a full-time Exchange president and the replacement of floor traders and specialists with a body weighted to house brokers.

In SEC v. Electric Bond and Share, the U.S. Supreme Court upheld the constitutionality of the Public Utility Holding Company Act. The Court deferred decision on the most controversial aspects of PUHCA, including the "death penalty" provision. Following the decision, utility companies began to register with the U.S. Securities and Exchange Commission, but refused to voluntarily divest and reorganize, requiring the SEC to litigate such cases.

The Chandler Act revised the National Bankruptcy Act to permit the U.S. Securities and Exchange Commission to assist federal courts in cases involving corporate reorganizations. The SEC's role in corporate bankruptcies was later circumscribed by Congress in the Bankruptcy Reform Act of 1978. The U.S. Supreme Court sustained the constitutionality of the Chandler Act in 1940 in SEC v. United States Realty and Improvement Co..

The Maloney Act, enacted on June 25, amended the Securities Exchange Act of 1934 to provide for the formation of a national association of brokers and dealers that would create and enforce disciplinary rules and promote just and equitable principles of trade. The U.S. Securities and Exchange Commission was provided with the power to review all disciplinary decisions and rules of this body.

The U.S. Securities and Exchange Commission struggled over accounting presentations it considered incorrect, accepting full disclosure of incorrect accounting rather than restatement. Accounting Series Release No. 4, Administrative Policy on Financial Statements, clarified that disclosure would be inadequate for accounting practices for which there was no substantial authoritative support or if the practice varied from a published SEC view. Through ASR No. 4, the SEC reserved the right to say who had substantial authoritative support, but opened the way to give that recognition to standards issued by the accounting profession.

In response to ASR No. 4, the American Institute of Accountants expanded its Committee on Accounting Procedure and gave it responsibility to issue pronouncements on accounting principles without the approval of the AIA membership or governing Council.

The U.S. Securities and Exchange Commission's exposure of the fraudulent financial statements of McKesson & Robbins, Inc., revealing significant fictitious items in sales, inventories and accounts receivable, was the most searching investigation to date by a government agency into independent audits and the practices of the audit profession. The following year, the American Institute of Accountants required auditors to observe inventories and confirm receivables when either was significant.

The Chandler Act, passed in 1938, tasked the SEC with helping ensure that bankrupt corporations were not taken over by incumbent insiders. The Commission delegated much of this work to the regional offices, which, due to proximity, were expected to maintain a close working relationship with the affected companies.

Enacted on August 3, the Trust Indenture Act supplemented the Securities Act of 1933 with respect to debt securities and their public distribution, containing a variety of provisions protecting the holders of debt securities covered by an indenture.

Under the terms of the Maloney Act, the National Association of Securities Dealers registered on August 7 as a self-regulatory organization. By year end, over 2,600 broker-dealer firms joined the NASD.

SEC Chairman William O. Douglas was appointed to the U.S. Supreme Court, forming a solid New Deal majority. He became the longest-serving Associate Justice to date, retiring in 1975.